ECB Tone Meter

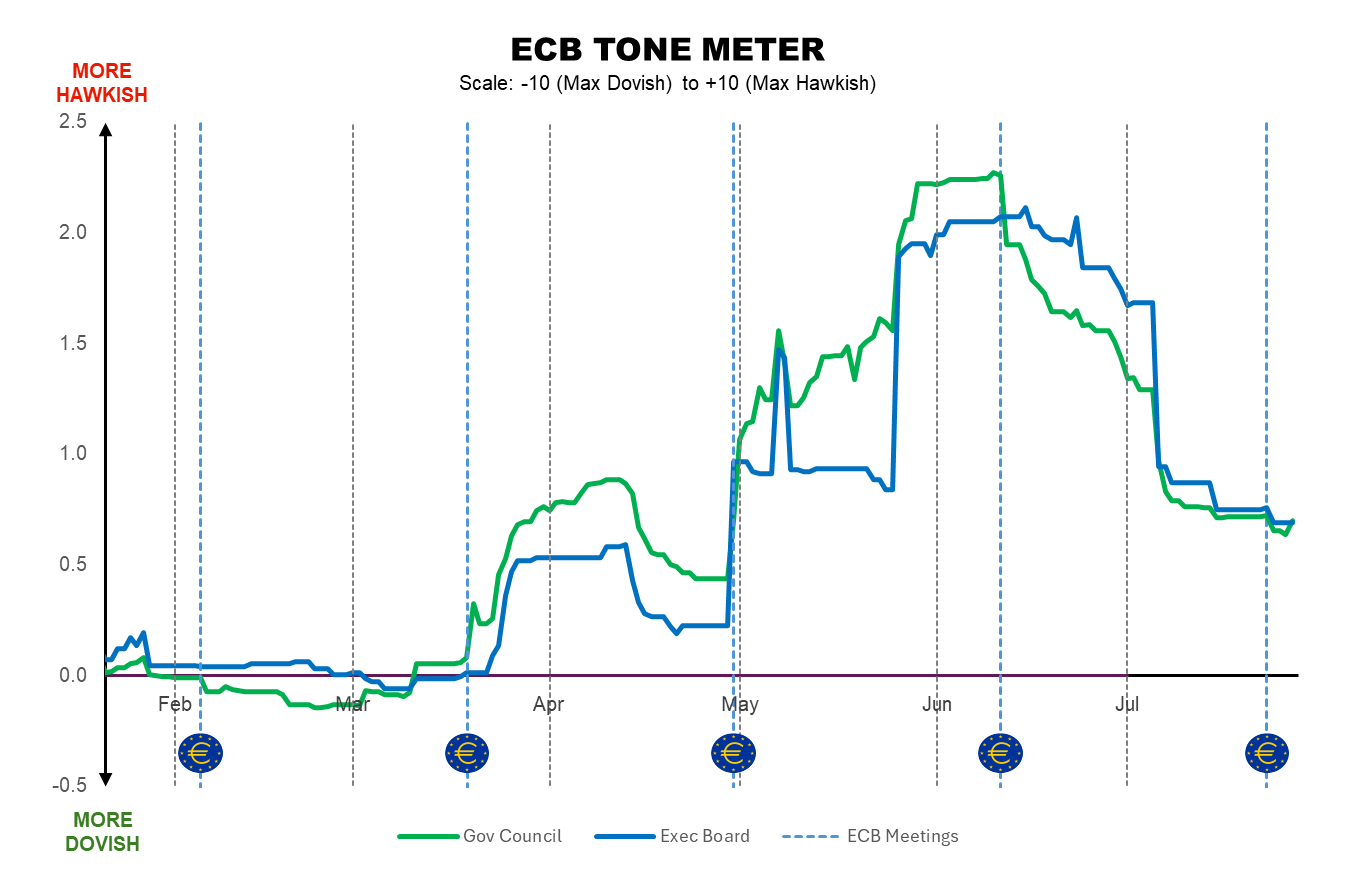

The ECB Tone Meter is an index measuring the overall dovishness or hawkishness of recent communications from the ECB Governing Council, factoring in all member public speeches and communications.

This provides a quantitative tool to summarize and analyze multiple qualitative inputs to provide a point estimate of the current tone, assess how it has evolved over time, and ultimately provide clues on potential future policy action.

Tone Snapshot

Entire Governing Council

27 Members0.7

Executive Board

6 Members0.69

Explainer - ECB Tone Meter Scores: The Tone Meter gauge displays values from -7.5 to +7.5. Technically the values could print outside this range (full scale is -10 to +10) but in practice the composite value rarely approaches these extremes, and a reduced range makes meaningful shifts more clearly visible. In practice, our experience gives the following as a rough interpretation of the values:

.png)

Tone Evolution

ECB Tone Meter Weekly Update: Cautious Post-July Messaging Brings Tone Closer to Neutral

By Marta Vilar – MADRID (Econostream) – Econostream’s ECB Tone Meter edged slightly lower this week in its Governing Council and Executive Board measures as policymakers struck a patient tone on further tightening while continuing to point to September as the next natural opportunity for reassessment.

24 July 2026Key Drivers of ECB Tone Meter Movements

Below is a breakdown of key periods, grouped by the dominant communication tone observed:

Hawkish Tone Returns After April Meeting Presser

- 30 April – Mid May: After the ECB press conference on April 30, Governing Council members again adopted conditional language suggesting that a rate hike could be possible in the near term. Latvia’s Mārtiņš Kazāks said the ECB would be forced to raise rates if inflation expectations deteriorated, while others, including Germany’s Joachim Nagel, said hikes would “become increasingly likely” if the inflation outlook failed to improve significantly.

Hawkish Tone Recedes as April Meeting Approaches

- 24 – 29 April: Policymakers no longer sounded convinced that an April rate hike was likely, citing positive developments in the war and the absence so far of visible second-round effects. President Christine Lagarde implied a more symmetric stance than markets had perceived, saying the ECB was “ready to move in the direction that is required.” The assessment of current conditions relative to the baseline also sounded less hawkish, with some, including Croatia’s Boris Vujčić, saying the situation remained “still very close to the baseline.” Many, such as Germany’s Joachim Nagel, emphasized that inflation expectations were still well anchored.

Post-Presser Triggers Hawkish Pivot

- 20 March – 13 April: Governing Council members turned increasingly hawkish after the March 19 press conference, with several governors suggesting that the next move was likely to be a rate hike, potentially as soon as the following meeting. Still, their remarks retained an element of conditionality. Among the most notable comments were those from Germany’s Joachim Nagel, who said an April hike would “probably be necessary” if certain “conceivable” conditions materialized, and Belgium’s Pierre Wunsch, who did not rule out a move as early as April.

Tone Moves Above Neutral Amid Iran Shock

- 1 – 19 March: After the outbreak of the war in Iran, the tone turned slightly more hawkish, as Governing Council members began suggesting that the ECB would act if the shock required it to preserve medium-term price stability. Among the more hawkish voices were Slovakia’s Peter Kažimír, who said a rate hike was “potentially closer” than many expected, and Latvia’s Mārtiņš Kazāks, who said a hike would be needed if there are concerns that the shock could raise inflation expectations.

Governing Council Heads Steadily to Slightly Below Neutral

- 16 January – 28 February: The tone of the ECB Governing Council remains close to neutral but is gradually shifting into dovish territory, below zero. The move reflects comments from Governing Council members suggesting that the next policy move could be downward. Among those signaling this view are Greece’s Yannis Stournaras and Malta’s Alexander Demarco. France’s François Villeroy de Galhau also struck an increasingly dovish tone, highlighting the predominance of downside risks.

Post-December Calm: Governing Council Tone Edges Hawkishly, But Only Slightly

- 19 December – 15 January: The ECB Governing Council’s tone remains in hawkish territory and ticks slightly higher. The move reflects modest hawkish shifts from policymakers such as Finland’s Olli Rehn and Estonia’s Madis Müller, who strike a more upbeat note on growth, alongside broader confirmation that current interest-rate levels are appropriate, as emphasized by Greece’s Yannis Stournaras and Portugal’s Álvaro Santos Pereira. The most striking development comes from Belgium’s Pierre Wunsch, who returns after two months of silence to say he has shed his dovish bias and is even open to a rate hike as the next step.

Methodology

Each comment made by an individual policymaker is assessed and assigned a score on a scale from +10 to -10, where +10 represents the most hawkish position and -10 the most dovish. Importantly, these scores are given in absolute terms, regardless of where the ECB is in the current monetary policy cycle and what the historical bias of each policymaker is.

In our ECB Tone Meter we include only remarks in which a policymaker’s personal stance is clearly expressed or can be confidently inferred. While we apply a consistent framework, we acknowledge that there is an inherent degree of subjectivity in interpreting tone and intent.

Still, our experience suggests that this approach captures policy shifts early and reliably. The result is a unique, real-time snapshot of the evolving policy mood in Frankfurt — helping you spot shifts, trends, and turning points as they happen.